Although this is a technical update referred to as an “expansion of tax brackets,” in practice it has a direct impact on monthly net income and tax coordination (tax adjustments).

What does the change mean?

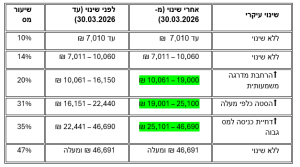

The income tax brackets of 20%, 31%, and 35% have been expanded. As a result, individuals earning from NIS 16,000 and above will receive an increase in their net salary of several hundred shekels per month.

Under the new brackets, taxpayers will move to the next tax bracket at a higher income level than before. In other words, the lower tax rate will now apply to a higher salary than previously.

We have summarized a comparison table of tax brackets before and after the change. This update improves the situation for salaried employees, nearly a year after the government decided not to index tax brackets to inflation—effectively imposing a “hidden tax” on the public.

The expansion of tax brackets applies retroactively from January 2026. This means that after updating payroll systems and recalculating salaries based on the new brackets, for some employees this will be reflected in the March 2026 payslip, and for others (whose salaries were already processed and paid) in the April 2026 payslip. This will result in a noticeable increase of several hundred shekels in net income.

How will this affect tax coordination (tax adjustments)?

As a reminder, this year the deadline for issuing tax coordination has been extended until May 13, 2026.

Those who have already issued a tax coordination and earn less than NIS 193,800 per year will not be affected by the change in tax brackets.

Employees earning above NIS 193,800 who have already completed tax coordination will have the necessary updates made automatically by the Tax Authority. They will only need to download the updated tax coordination and submit it to their employer(s).

Employees who have not yet issued a tax coordination (because last year’s approval was extended) are required to do so. However, there is no need to rush immediately—you are expected to receive a notification from the tax coordination system once it has been updated according to the new legislation. The update may be delayed due to the holidays.

In any case, make sure to issue your 2026 tax coordination by May 13, 2026.

The “Assistance to Parents of Children up to Age 3 (Legislative Amendments), 2024” law has come into effect. According to the law, starting from the 2024 tax year, additional tax credit points (!) will be calculated for parents for each child from the year of birth until the year the child turns 3, as follows:

- For each child in the year of birth, one tax credit point will be added for each parent.

- For each child who is one or two years old in the tax year, 2 tax credit points will be added for each parent.

- For each child who turns three years old in the tax year, one tax credit point will be added for each parent.

Since typically women’s income decreases in the tax year in which they give birth and they do not utilize the tax credit points due to low tax liabilities, Income Tax allows the woman to transfer one out of the 2.5 points she is entitled to, to the next tax year.

Note: The additional tax credit points are for both parents! For example, two parents of a two-year-old child will receive an additional 4 tax credit points. If they meet the relevant tax liabilities, they will benefit monthly from the following addition: (2+2) * 242 = 968 NIS (242 NIS is the value of a tax credit point in 2024).

The amendment to the law is retroactive from 01/01/24, and parents will see a significant increase in their net salary starting from the 4/24 payslip. Attached is a comparison table of tax credit points before and after the change.